Step-Up SIP Strategy: Scale Your Mutual Fund Investments in 2026

Most investors set up a SIP and forget it — same amount, year after year. But as your income grows, your wealth creation potential stays frozen. The Step-Up SIP strategy is the upgrade your investment plan may be missing.

A Step-Up SIP (also called a Top-Up SIP) lets you increase your monthly investment periodically — typically every year — so your portfolio grows in lockstep with your income. The result: a potentially much larger corpus over time, without requiring any drastic financial changes upfront.

What You Will Learn

- What Step-Up SIP is and how it works

- The Step-Up SIP formula and illustrative calculation

- When and how to increase your SIP amount

- Portfolio diversification rules for scaled SIPs

- Tax implications of increasing SIP investments

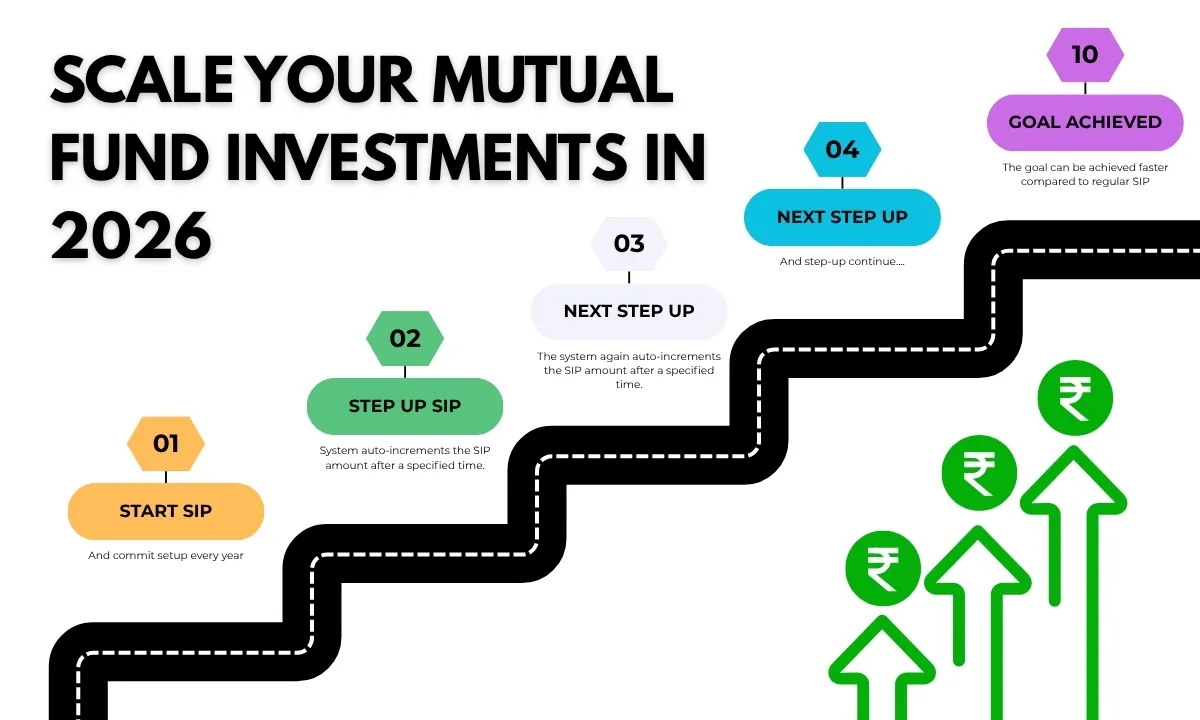

What Is a Step-Up SIP?

A Step-Up SIP is a systematic investment plan where you commit — in advance — to increasing your instalment by a fixed rupee amount or a fixed percentage at a set interval, usually annually.

Example:

- You start a SIP of ₹10,000/month in January 2026.

- You commit to a 10% annual step-up.

- By January 2027, your SIP becomes ₹11,000/month.

- By January 2028, it becomes ₹12,100/month, and so on.

This is different from manually increasing your SIP whenever you feel like it. A Step-Up SIP is a pre-committed, automated escalation — which removes the temptation to delay the increase.

Most major mutual fund platforms and fund houses support this feature, sometimes labelled as a Top-Up SIP.

The Step-Up SIP Formula: How the Numbers Work

The mathematics behind a Step-Up SIP is more nuanced than a regular SIP, because both the instalment amount and the compounding base change each year.

The simplified version of the Step-Up SIP future value formula is:

FV = Sum of FV of each annual tranche, where each tranche’s instalment increases by the step-up rate

Rather than work through the full formula manually, investors may use a Step-Up SIP calculator, which is available on most fund platforms.

Illustrative Comparison (Not a Guaranteed Outcome)

| Strategy | Starting SIP | Annual Step-Up | Tenure | Assumed CAGR | Illustrative Corpus |

|---|---|---|---|---|---|

| Regular SIP | ₹10,000/month | Nil | 20 years | 12% p.a. | ~₹99.9 lakhs |

| Step-Up SIP | ₹10,000/month | 10% p.a. | 20 years | 12% p.a. | ~₹1.9 crore |

| Step-Up SIP | ₹5,000/month | 15% p.a. | 20 years | 12% p.a. | ~₹1.5 crore |

⚠️ Important: These figures are purely illustrative, based on a constant assumed rate of return. Actual mutual fund returns vary with market conditions and are not guaranteed. Past performance may or may not be sustained.

The key insight: a 10% annual step-up on a ₹10,000 SIP can approximately double the potential corpus compared to a flat SIP over 20 years — for the same starting investment and holding period.

When and How to Increase Your SIP Amount

Knowing when to trigger your step-up is as important as the mechanics. Common, practical triggers include:

1. Annual Salary Increment

The most natural trigger. If you receive a 10–12% raise, committing even half of that incremental income to your SIP keeps your lifestyle inflation in check while accelerating wealth creation.

2. Bonus or Windfall

A Diwali bonus, performance incentive, or freelance income can be partially deployed as a one-time SIP top-up or to fund the increased instalment for the next 12 months.

3. EMI Reduction

When a loan — a car EMI, personal loan, or home loan — closes, the freed-up cash flow is an ideal source for a step-up. You were already living without that money; redirect it to investments.

4. Pre-Committed Annual Escalation

The simplest approach: set up a 10% or 15% automatic annual step-up when you start the SIP. No decision fatigue, no delays.

The suitability of any step-up frequency or amount depends on your personal cash flows, financial obligations, and investment goals. Investors may evaluate these options in consultation with their financial adviser.

Portfolio Diversification for a Scaled Step-Up SIP

As your SIP amounts grow larger, portfolio construction becomes more important. Over-diversification — holding 15 or 20 funds — adds complexity without meaningfully reducing risk, and can dilute returns.

A Balanced Framework

| Category | Role | Suggested Allocation |

|---|---|---|

| Large Cap or Flexi-Cap Fund | Core stability, broad market exposure | 35–45% |

| Mid Cap Fund | Growth potential, moderate volatility | 20–30% |

| Small Cap Fund | Higher growth, higher risk | 10–15% |

| Hybrid or Balanced Advantage Fund | Volatility buffer, auto-rebalancing | 10–20% |

| Debt or Short Duration Fund | Capital preservation, short-term goals | 5–15% |

Note: The above is an illustrative framework, not a recommendation. The appropriate allocation depends entirely on an investor’s risk profile, investment horizon, age, and financial goals. Investors may consult an AMFI-registered distributor to build a personalised portfolio.

Key Diversification Principles

- 3 to 5 schemes is generally sufficient for a well-structured retail portfolio.

- Avoid holding multiple funds within the same sub-category (e.g., three large-cap funds), as they tend to hold overlapping stocks.

- Review portfolio overlap annually using a fund overlap tool.

- As your corpus grows — especially beyond ₹50 lakhs — the role of asset allocation becomes more critical than fund selection.

Tax Implications of Scaling Your SIP

Each SIP instalment — including each stepped-up instalment — is treated as a separate purchase for capital gains tax purposes. This has practical implications:

Equity Mutual Funds

| Holding Period | Tax Treatment |

|---|---|

| More than 12 months | Long-Term Capital Gains (LTCG) — 12.5% above ₹1.25 lakh aggregate |

| Up to 12 months | Short-Term Capital Gains (STCG) — 20% |

Debt Mutual Funds (for units purchased on or after 1 April 2023)

- Gains are taxed as per the investor’s income tax slab, regardless of the holding period.

- Indexation benefits are no longer available for debt fund units purchased from 1 April 2023 onwards.

Practical Tax Planning Considerations

- Because each monthly instalment has its own 12-month clock, partial redemptions can be structured to prioritise units held for more than 12 months (older units are typically redeemed first using FIFO — First In, First Out — as per tax rules).

- For investors in higher tax brackets, the interplay between LTCG, STCG, and debt fund taxation is worth reviewing with a qualified tax adviser, especially as the corpus grows.

- ELSS funds (Equity Linked Savings Scheme) offer a tax deduction of up to ₹1.5 lakh under Section 80C but come with a mandatory 3-year lock-in per instalment. Step-Up SIPs in ELSS are possible but each stepped-up instalment has its own 3-year lock-in period.

Tax laws are subject to change. Investors may consult a qualified tax advisor for their specific circumstances.

Building a ₹1 Crore Corpus: Illustrative Scenarios

The ₹1 crore target is a common milestone for Indian retail investors. Here are illustrative Step-Up SIP scenarios that may reach that level — note that outcomes depend entirely on actual market returns:

| Starting SIP | Annual Step-Up | Assumed CAGR | Approximate Tenure to ₹1 Cr |

|---|---|---|---|

| ₹5,000/month | 10% p.a. | 12% p.a. | ~18 years |

| ₹10,000/month | 10% p.a. | 12% p.a. | ~14 years |

| ₹15,000/month | 10% p.a. | 12% p.a. | ~12 years |

| ₹10,000/month | Nil (regular SIP) | 12% p.a. | ~20 years |

⚠️ These are purely illustrative calculations at a constant assumed rate of return. Mutual fund returns are not guaranteed and vary with market conditions.

The table highlights the core principle: starting earlier and increasing contributions consistently are among the most controllable levers an investor has — market returns are not.

Common Mistakes to Avoid

- Stopping the SIP at the first sign of market volatility. Short-term declines are a normal part of equity investing; they also mean units are purchased at lower prices, which can benefit long-term compounding.

- Delaying the step-up indefinitely. Each year of delay reduces the compounding runway. A pre-committed annual step-up removes this friction.

- Ignoring asset allocation as the corpus grows. A portfolio appropriate at ₹5 lakhs may need rebalancing at ₹50 lakhs.

- Treating Step-Up SIP as a replacement for goal-based financial planning. A Step-Up SIP is a powerful tool, but it works best when tied to a specific goal, time horizon, and risk profile.

Key Takeaways

- A Step-Up SIP increases your monthly instalment periodically — typically annually — aligning investments with growing income.

- Even a 10% annual step-up can potentially double the corpus compared to a flat SIP over a 20-year horizon (illustrative only; not guaranteed).

- Practical triggers include annual salary increments, bonus income, and closed EMIs.

- A portfolio of 3–5 funds across large-cap, mid-cap, and hybrid categories is generally sufficient; avoid over-diversification.

- Each SIP instalment has its own capital gains clock; LTCG at 12.5% applies to equity fund units held over 12 months.

- Pre-committing to a step-up removes the temptation to postpone increases and is the most effective way to implement this strategy.

Conclusion

The Step-Up SIP strategy is one of the more practical and accessible tools available to Indian retail investors for long-term wealth creation. It does not require market timing, complex analysis, or large upfront capital — just a commitment to grow your investment in line with your growing income.

Investors may evaluate whether a Step-Up SIP structure aligns with their financial goals, cash flows, and risk profile. The appropriate starting amount, step-up percentage, fund selection, and tenure are individual decisions best made with a clear understanding of one’s own financial circumstances.

If you would like to explore how a Step-Up SIP might fit into your broader financial plan, Meta Investment — an AMFI-registered mutual fund distributor based in Pune — can help you structure a goal-based investment plan tailored to your needs.

Interested in Investing? Connect with Meta Investment

Meta Investment is a financial product distribution and services firm. If you'd like to explore whether a financial product is the right fit for your portfolio, our team will walk you through the details, help you assess suitability, and guide you through the onboarding process.

🔗 Download the Meta Investment App & Begin Today

Mutual Fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance may or may not be sustained in the future.

This communication is intended solely for educational and informational purposes and should not be construed as investment advice, a recommendation, or a solicitation to buy or sell any financial product. The suitability of any investment category depends on an investor’s financial goals, risk appetite, investment horizon, and overall financial circumstances. Investors may consult their Mutual Fund Distributor or Financial Advisor before investing.

Returns less than 1 year are absolute; greater than 1 year are CAGR. Illustrative corpus figures are based on assumed constant rates of return and are not indicative of actual or expected returns. If investments are made through a mutual fund distributor, the distributor may receive commissions from Asset Management Companies.

Meta Investment – Your Investment and Insurance Companion.

Frequently Asked Questions

What is a Step-Up SIP?

A Step-Up SIP (also called a Top-Up SIP) is a variant of a Systematic Investment Plan where you commit to increasing your SIP instalment by a fixed amount (e.g., ₹500) or a fixed percentage (e.g., 10%) at a pre-defined interval, typically annually. This allows your investments to grow in line with your rising income, accelerating wealth creation over time.

How does a Step-Up SIP differ from a regular SIP?

In a regular SIP, the instalment amount stays constant throughout the tenure. In a Step-Up SIP, the amount increases periodically. Because of the higher contributions in later years — when compounding has also been working longer — a Step-Up SIP can generate a significantly larger corpus than a regular SIP with the same starting amount over the same period.

What is the Step-Up SIP formula?

The future value of a Step-Up SIP is calculated using a modified future value formula that accounts for the annual increase in instalment. While the exact formula is complex, most mutual fund platforms offer Step-Up SIP calculators. The key variables are: starting monthly SIP amount, annual step-up percentage or amount, expected rate of return, and investment tenure in years.

How much can a 10% annual step-up make a difference?

Illustratively, a ₹10,000/month regular SIP over 20 years at an assumed 12% p.a. CAGR may grow to approximately ₹99.9 lakhs. The same SIP with a 10% annual step-up (starting at ₹10,000 and increasing each year) may grow to approximately ₹1.9 crore over the same 20-year period — nearly double the corpus. Note: These are illustrative figures only. Actual returns depend on market conditions and are not guaranteed.

When should I increase my SIP amount?

Common triggers for increasing your SIP include: receiving an annual salary increment, a bonus or windfall, reduction in a major EMI or expense, or simply at a fixed annual interval as part of a pre-committed step-up plan. The key principle is to let your investments grow in proportion to your growing income.

How many mutual fund schemes should I hold in a Step-Up SIP portfolio?

Over-diversification can dilute returns without meaningfully reducing risk. A well-structured SIP portfolio of 3 to 5 carefully chosen funds across different categories (e.g., large cap, flexi-cap, mid cap, and one debt or hybrid fund) is generally considered sufficient for most retail investors. The suitability of any specific combination depends on your goals, risk profile, and investment horizon.

What are the tax implications of increasing my SIP amount?

Each SIP instalment is treated as a separate investment for capital gains tax purposes. Equity mutual fund units held for more than 12 months attract Long-Term Capital Gains (LTCG) tax at 12.5% (above ₹1.25 lakh aggregate in a financial year). Units sold within 12 months attract Short-Term Capital Gains (STCG) tax at 20%. For debt mutual funds, gains are taxed as per the investor's income tax slab regardless of holding period. Investors may consult a tax advisor for their specific situation.

Can I pause or stop a Step-Up SIP if needed?

Most mutual fund platforms allow you to pause, reduce, or stop a Step-Up SIP, subject to the fund house's terms. The existing units remain invested and continue to grow. However, frequent interruptions reduce the effectiveness of the compounding and rupee-cost-averaging benefits the strategy is designed to deliver.

Is Step-Up SIP suitable for NRI investors?

Yes, NRI investors can invest in mutual funds via SIP (including Step-Up SIPs) through NRE or NRO accounts, subject to FEMA regulations and fund-house policies. NRIs from certain countries (such as the USA and Canada) may face restrictions from specific fund houses. NRI investors may consult an AMFI-registered distributor or tax advisor familiar with cross-border investment rules before investing.

How do I start a Step-Up SIP?

You can start a Step-Up SIP through an AMFI-registered mutual fund distributor or directly on a mutual fund platform. You typically select the scheme, enter your starting SIP amount, choose the step-up frequency (annual), enter the step-up amount or percentage, and set the tenure. An AMFI-registered distributor like Meta Investment can help you structure the right plan based on your financial goals and risk profile.

Mutual fund updates, SIP tips, and what's moving the market. No daily noise — only when there's something worth reading.

Read more about

- Financial Planning Checklist for Indian IT Employees Facing the 2026 Hiring Slowdown

- Master Your Financial Future with Our Expert-Led Webinars

- Mutual Fund & Financial Planning Services in Sambhaji Nagar, Pimpri Chinchwad

- Mutual Fund, NPS & Financial Planning Services in Baner, Pune

- Corporate NPS for Companies in Bhosari Industrial Area, Pune

- Mutual Fund Distributor & Financial Planner in Pune

- Mutual Fund & Financial Planning Services in Chinchwad, Pune

- Corporate NPS in Pune: Setup for Companies | Meta Investment

- Mutual Fund Distributor & Financial Planner in Pimple Saudagar, Pune

- Mutual Fund & Financial Planning Services in Hingewadi, Pune

- Mutual Fund & Financial Planning Services in Pimpri Chinchwad, Pune

- Mutual Fund & Financial Planning Services in Balewadi, Pune

- Mutual Fund & Financial Planning Services in Rahatani, Pune

- Mutual Fund & Financial Planning Services in Wakad, Pune

- म्युच्युअल फंड भारतात 2026: प्रकार, SIP परतावा आणि निवड मार्गदर्शिका

- PMS vs Mutual Funds: Detailed Comparison for HNI Investors (2026)

- SIP vs Lumpsum: Which Should You Choose?

- म्युच्युअल फंड मधील SIP म्हणजे काय? फायदे, काम करण्याची पद्धत (२०२५)

- २०२५ साठी भारतातील सर्वोत्तम कर बचत पर्याय | सेक्शन ८०सी आणि इतर

- Thank you for registering!

")