Rupee Depreciation and the Rising Cost of Your Child's Dream Abroad

Planning to fund your child’s overseas education? The rupee’s steady fall means the real cost is far higher than the college brochure suggests — here’s how to stay ahead.

You saved diligently. You budgeted for tuition, accommodation, and living expenses based on the university’s fee page. But when it was finally time to transfer money, you realised something sobering — the rupee had quietly eroded a significant chunk of your savings without you doing anything wrong.

This is the hidden tax that most Indian parents don’t account for when planning for international education: currency risk.

Sending a child to the US, UK, Europe, or Singapore is not just a financial goal — it is one of the largest single expenditures a middle-class or upper-middle-class Indian family will ever make. And unlike a home loan or a retirement corpus, this goal has a hard deadline. Your child’s admission letter does not wait for the rupee to recover.

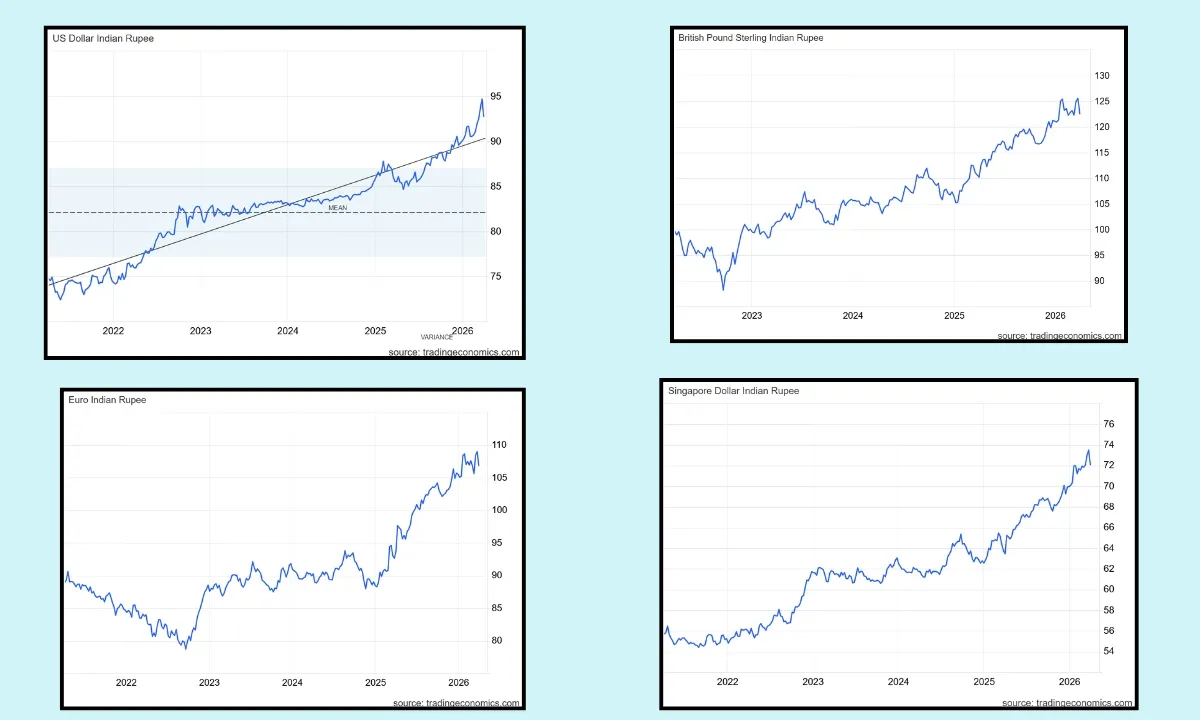

What the Charts Are Telling Us

The currency charts paint a clear, uncomfortable picture. Here’s how the Indian Rupee has moved against major currencies over the last four years:

- USD/INR: From around ₹74 in early 2022 to nearly ₹95 today — a depreciation of roughly 28%.

- GBP/INR: From around ₹90–95 in late 2022 to approximately ₹124–125 today — up nearly 35%.

- EUR/INR: From lows of around ₹79 in mid-2022 to roughly ₹107–110 today — a rise of nearly 40%.

- SGD/INR: From around ₹55–56 in 2021–22 to approximately ₹73–74 today — an increase of over 32%.

Notice the pattern: every single major currency has strengthened against the rupee — and the trend is not a sudden event, it is a slow, persistent, structural drift.

What this means in practice is stark. If you had estimated that a four-year undergraduate programme in the UK would cost ₹80 lakhs in 2022, that same programme — with the same fee in pounds — costs closer to ₹1.1 crore today. That is ₹30 lakhs more, not because the university raised its fees, but simply because the rupee got weaker.

Why the Rupee Keeps Falling — And Why It Will Likely Continue

India’s rupee depreciation is not accidental. It is driven by structural factors that are unlikely to reverse in any meaningful way over the medium term:

- Inflation differential: India consistently runs a higher inflation rate than the US, UK, or Europe. Over time, this erodes the rupee’s purchasing power relative to those currencies.

- Trade deficit: India imports far more than it exports (especially oil), keeping persistent demand for foreign currency.

- RBI’s managed float: The Reserve Bank of India does not let the rupee float freely — it manages the pace of depreciation — but the direction has historically been one-way.

- Global risk sentiment: During periods of global uncertainty, capital flows out of emerging markets like India and into “safe haven” currencies like the USD, accelerating rupee weakness.

Historically, the rupee has depreciated against the dollar at roughly 3–4% per year on average. For a goal that is 8–10 years away, this compounding effect is enormous.

The Math Your Insurance Agent Didn’t Show You

Let’s say your child is 8 years old today, and you want to build a corpus for a 2-year postgraduate programme in the US starting in 2033. Current estimated cost: $60,000 (roughly ₹57 lakhs at today’s rate of ~₹95).

But if the rupee depreciates even modestly at 3% per year, by 2033 the dollar could be at ₹117–120. That same $60,000 programme would cost you ₹72–75 lakhs — a difference of ₹15–18 lakhs, doing nothing but sitting in a rupee-denominated fixed deposit.

This is precisely why saving in rupees alone for a foreign currency goal is like running on a treadmill — you may be putting in effort, but you’re not actually covering ground.

Why International Investing Is Not Optional for This Goal

The most logical hedge against rupee depreciation for an international education goal is to hold at least a portion of your savings in assets denominated in or linked to foreign currencies. This way, as the rupee falls, the INR value of your investment rises — naturally offsetting the increasing cost.

International investing for this goal serves two purposes simultaneously:

- Currency hedge — your corpus grows in rupee terms as foreign currencies appreciate.

- Wealth creation — global equity markets (especially the US) have delivered strong long-term returns, diversifying your portfolio beyond Indian equities.

Historically, Indian investors who held US equity funds saw their returns amplified by rupee depreciation. A fund that returned 10% in dollar terms could have delivered 13–14% in rupee terms, simply because of currency movement.

For a goal like international education, this is not speculation — it is goal-aligned investing.

A Note on GIFT City — A New Avenue Worth Knowing

India’s GIFT City (Gujarat International Finance Tec-City) has emerged as a regulated gateway for Indian residents to access international investment products without the complexity of remitting money under the Liberalised Remittance Scheme (LRS).

Several fund houses now offer retail-oriented international mutual funds structured out of GIFT City’s IFSC, allowing Indian investors to participate in global markets — including US equities, global indices, and multi-asset international strategies — in a compliant and relatively accessible manner. These funds are regulated by IFSCA (the GIFT City regulator) and are increasingly being made available through mainstream distribution channels.

For a parent building a corpus for overseas education, GIFT City-based funds offer a convenient way to build genuine foreign currency exposure as part of a structured investment plan. This is an evolving space, and speaking with a qualified advisor before investing is advisable — but it is certainly a space worth tracking.

Building a Practical Plan: What Should You Do?

You don’t need to move everything overseas. A balanced, goal-oriented approach works best:

| Component | Purpose | Example Instruments |

|---|---|---|

| Indian Equity (Flexi-cap / Midcap) | Long-term wealth creation in INR | Mutual Funds / PMS |

| International Equity Funds | Currency hedge + global growth | US Index Funds, GIFT City funds |

| Debt / Hybrid | Capital preservation as goal nears | Short-duration debt funds, FDs |

| FX-linked instruments | Direct currency exposure | International fund of funds |

A thumb rule often used: allocate at least 30–40% of your international education corpus to foreign-currency-linked assets, gradually shifting to safer instruments as the goal approaches (typically 2–3 years before the child leaves).

Starting early is the single biggest advantage you have. A SIP of ₹15,000 per month in a mix of Indian and international equity funds, started when your child is 7–8 years old, can build a meaningful corpus by the time they turn 18 — one that has also benefited from rupee depreciation rather than been hurt by it.

Key Takeaways

- The rupee has depreciated 28–40% against major education destination currencies in just the last 4 years — and this trend is structural, not temporary.

- An education goal priced in USD, GBP, EUR, or SGD is a foreign currency liability and must be treated as one.

- Saving in rupee-only instruments for a foreign currency goal leaves you exposed to a risk that compounds silently over years.

- International mutual funds — including newer options available through GIFT City — offer accessible, regulated ways to build foreign currency exposure.

- The best time to start this kind of planning was five years ago. The second best time is today.

Conclusion

Your child’s dream of studying abroad is worth planning for seriously — and that planning has to account for the world as it is, not as we wish it were. The rupee will likely be weaker in 2030 than it is today. The question is whether your savings will have kept pace, or whether you’ll be scrambling to make up the difference.

A thoughtfully constructed portfolio — one that looks beyond Indian borders and accounts for currency risk from day one — can make the difference between stress-free funding and a last-minute shortfall.

Let’s plan this right.

Interested in Investing? Connect with Meta Investment

Meta Investment is a financial product distribution and services firm. If you'd like to explore whether a financial product is the right fit for your portfolio, our team will walk you through the details, help you assess suitability, and guide you through the onboarding process.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Mutual fund investments are subject to market risks. International investments carry additional currency and geopolitical risks. Please consult a SEBI-registered financial advisor before making investment decisions.

Frequently Asked Questions

How does rupee depreciation affect the cost of my child's overseas education?

When the rupee weakens against the currency of your child's study destination, the INR amount you need to pay the same foreign-currency fees goes up — even if the university hasn't raised its fees at all. For example, the rupee has depreciated nearly 28% against the US dollar and over 35% against the British pound in just the last four years. This means a course that cost ₹80 lakhs in 2022 could cost ₹1.1 crore or more today, simply due to currency movement.

Is rupee depreciation a temporary problem or a long-term trend?

It is a long-term structural trend. India's consistently higher inflation rate relative to developed economies, its trade deficit, and global capital flow patterns have caused the rupee to depreciate against major currencies at roughly 3–4% per year on average historically. While the RBI manages the pace, the direction has persistently been one-way. Parents planning 8–10 years ahead should factor this into their education corpus calculations from the start.

Why is saving only in rupee-denominated instruments a problem for an overseas education goal?

An overseas education goal is essentially a foreign currency liability — the fees are priced in USD, GBP, EUR, or SGD. If your savings are entirely in rupee instruments like FDs or Indian mutual funds, the value of your corpus in foreign currency terms shrinks every year as the rupee depreciates. You may be saving diligently in INR, but the purchasing power of that corpus in the destination country is quietly eroding.

How much of my education corpus should be in international or foreign-currency-linked investments?

A common approach is to allocate 30–40% of the education corpus to foreign-currency-linked assets such as international equity mutual funds or global index funds. The remaining portion can stay in Indian equity and debt instruments for growth and stability. As the goal gets closer — typically 2–3 years before your child is due to leave — the allocation should gradually shift toward lower-risk instruments to protect the corpus from short-term market volatility.

What are international equity mutual funds and how do they help?

International equity mutual funds are Indian mutual fund schemes that invest in stocks or indices of overseas markets — primarily the US, but also Europe, Asia, and global indices. They are priced in INR but the underlying assets are in foreign currency. This means when the rupee depreciates, the INR value of these funds tends to rise, naturally hedging your education goal against currency risk while also giving your portfolio exposure to global growth.

What is GIFT City and how is it relevant to investing for overseas education?

GIFT City (Gujarat International Finance Tec-City) is India's regulated international financial services hub. Several fund houses have launched retail-oriented international mutual funds structured out of GIFT City's IFSC (International Financial Services Centre), regulated by IFSCA. These funds allow Indian resident investors to access global markets in a compliant manner, building genuine foreign currency exposure without the complexity of remitting money abroad under the LRS. For an international education goal, GIFT City-based funds are an emerging and accessible option worth exploring with your financial advisor.

When should I start investing for my child's overseas education goal?

The earlier the better. Starting when your child is 7–8 years old gives you a 10-year runway, which allows compounding to work fully and gives you time to ride out short-term market volatility. A monthly SIP of ₹15,000–₹20,000 spread across Indian and international equity funds, started early, can build a meaningful corpus by the time your child turns 18 — one that has also benefited from rupee depreciation rather than been hurt by it.

Does investing internationally involve extra risk?

Yes, international investments carry additional risks including currency fluctuation (which can work both ways), geopolitical events, and differences in market regulation. However, for a goal that is itself priced in a foreign currency, having some international exposure actually reduces your overall goal risk — you are matching your assets to your liability. The key is to invest through regulated, SEBI-registered or IFSCA-regulated fund structures and to maintain a diversified portfolio rather than concentrating everything in a single market.

Can I use a child plan or endowment policy to save for overseas education?

Traditional child insurance plans and endowment policies are typically rupee-denominated, offer modest returns (often 5–6% CAGR), and provide no currency hedge for an overseas education goal. Given that the rupee depreciates 3–4% per year on average, a 5–6% return in rupees barely keeps pace with currency erosion — let alone inflation and rising tuition costs. A portfolio of equity mutual funds with some international allocation, combined with a separate term insurance cover, typically offers better outcomes for this goal.

How do I estimate how much corpus I need for my child's overseas education?

Start with the current estimated cost of the programme in the destination currency (tuition + living expenses). Then apply two adjustments: first, annual tuition inflation in that country (typically 3–5%); and second, the expected rupee depreciation over your investment horizon (historically 3–4% per year against the dollar). The combined effect means your INR target corpus should be significantly higher than a simple today's-rate calculation suggests. A financial advisor can help you model this with realistic assumptions based on your child's likely destination and timeline.

Mutual fund updates, SIP tips, and what's moving the market. No daily noise — only when there's something worth reading.

Read more about

- Aashadhi Ekadashi: Begin Your Journey to True Financial Samruddhi

- Financial Planning Checklist for Indian IT Employees Facing the 2026 Hiring Slowdown

- Master Your Financial Future with Our Expert-Led Webinars

- Mutual Fund Distributor & Financial Planner in Pune

- Mutual Fund, NPS & Financial Planning Services in Baner, Pune

- Mutual Fund & Financial Planning Services in Sambhaji Nagar, Pimpri Chinchwad

- Corporate NPS for Companies in Bhosari Industrial Area, Pune

- Mutual Fund & Financial Planning Services in Pimpri Chinchwad, Pune

- Mutual Fund & Financial Planning Services in Chinchwad, Pune

- Mutual Fund & Financial Planning Services in Wakad, Pune

- Mutual Fund & Financial Planning Services in Hingewadi, Pune

- Mutual Fund & Financial Planning Services in Balewadi, Pune

- Mutual Fund Distributor & Financial Planner in Pimple Saudagar, Pune

- Mutual Fund & Financial Planning Services in Rahatani, Pune

- Corporate NPS in Pune: Setup for Companies | Meta Investment

- Investment Options in India (2026): Where Should Your Money Go?

- NPS vs Mutual Funds: Which is Better for Retirement in India? (2026)

- PMS vs Mutual Funds: Detailed Comparison for HNI Investors (2026)

- Portfolio Management Services (PMS) in India | Guide for HNIs & NRIs

- Best Tax Saving Options in India for 2025 | Section 80C & More

- The Wealth Waari: Lessons in Discipline from a Timeless Journey

")